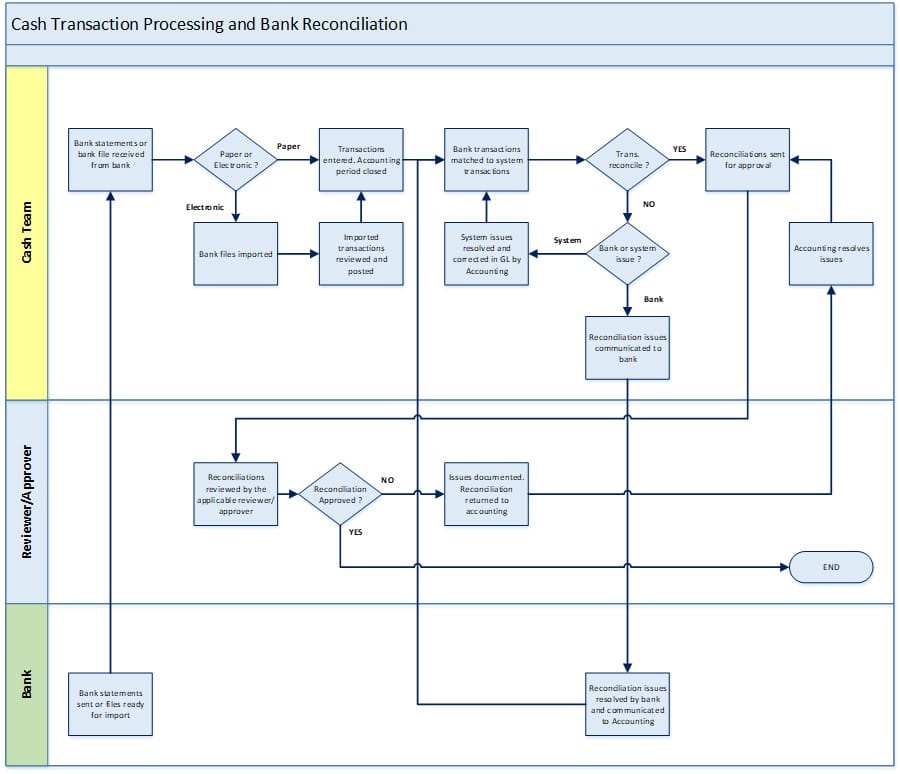

Bank Transaction Processing and Reconciliation

Use ERP functionality and bank tools to streamline cash transaction processing and increase cash control.

Use ERP functionality and bank tools to streamline cash transaction processing and increase cash control.

Table of Content

Processing bank transactions is an important company activity. Businesses receive and disburse cash and checks daily.

Accurate and controlled cash processing assists the company in determining its open Accounts Receivable (AR) and expected cash receipts, Accounts Payable (AP) check processing and upcoming cash obligations and in forecasting it’s cash position. Accurate and timely transaction processing and reconciliation can also play a role in reducing cash loss risk.

Daily bank transaction entry and cash application are usually processed and entered into the GL by a specific accountant. Today, all commercial banks provide transaction files in an electronic format, and ERPs support the import of these files. Use these capabilities to streamline cash transaction processing, as they help to ensure that all transactions are accounted for and assist in increasing transaction processing accuracy.

Whether manually processed or imported, any major bank transactions and “short pay” customer payments should be quickly identified and communicated to the applicable personnel for review, approval and issue resolution.

Bank reconciliations are assigned to and completed by a specific accountant. Ideally, the reconciliation should be completed by someone other than the accountant processing the cash transactions. In smaller companies where the same person completes both tasks, be sure that the reconciliation is reviewed by a senior accounting executive, or the outside accountant.

Be sure that bank account reconciliations are completed in a timely manner. Bank reconciliations should be completed monthly. Bank reconciling items need to be researched and resolved within 30 days from the period close. All bank reconciliations should be reviewed and approved by a senior accounting executive or the outside accountant.

Measures and alerts are meant to assist the user in keeping abreast of processing status, identifying anomalies, and ensuring that implemented process controls are effectively employed. The information below illustrates the interaction between bank transaction processing functionality, measures and alerts.

Functionality- ERP GL and Cash sub-ledger.

Measures and Alerts- Bank transactions more than “N” dollars.

Large bank transactions in excess of a certain amount can indicate a bank issue, or in some instances, illegal activity. It’s important to immediately review these transactions to ensure their accuracy, and to determine that the proper source documentation and approvals are in place.

Set the alert dollar limit to fit the size of your company. If you set the limit too high, you may not have the visibility you need. Set it too low, and you’ll be reviewing transactions which can be addressed in the bank reconciliation process. Use the alert in conjunction with sound accounting internal controls and timely transaction posting and reconciliation.

Remember, anyone engaging in illegal activities, such as embezzlement, rarely does so in a single transaction. Instead, they use smaller amounts in multiple transactions over a period of time, so recognize that fact when setting the dollar limit.

Measures and Alerts- JEs posted directly to cash GL accounts from outside the Cash sub-ledger.

There should be very few GL journal transactions posted directly to the Cash sub-ledger. Cash transactions are usually auto-posted from activities such as AP check processing, AR customer payments received and bank transaction importing or manual entry into the cash sub-ledger.

In cash accounts, GL journal entries are usually made to record some type of a correction, such as reclassing a miscode. Sometimes, GL journal entries are prepared to record manual checks from manual check account when the company wants to keep payment details confidential.

Since the journal transactions will not be included in the bank statement, they will be bank reconciliation open items. Be sure to review each of the entries identified. If they’re correct great, if they are incorrect, handle the issue in the bank reconciliation process.

Measures and Alerts- System bank reconciliations not completed “N” days past period end.

As I mentioned in the overview, timely bank reconciliations are important in effectively controlling the cash handling process. Bank reconciliations should be completed within 30 days of the period close. The problem in completing bank reconciliations later than 30 days is that any transaction errors are not resolved in a timely manner and can have a negative effect on cash planning and financial reporting later on.

I can’t overstate the importance of timely bank reconciliations. I can tell you from “hands on” experience, that having to explain a banking issue correction 60 or 90 days after its occurrence, is not a pleasant task, especially when it affects the income statement.

Since automated bank reconciliation is standard ERP functionality and completes most of the reconciliation tasks for the user, there really aren’t any excuses for reconciliations not being completed in a timely manner.

Measures and Alerts- “Short pay” Accounts Receivable cash application transactions more than “N” dollars.

When a customer short pays an invoice, there is usually a reason behind it. The customer may be unhappy with the services provided, has a billing issue of some sort, or some other problem.

The reason that short pay transactions should be reviewed is to identify the issue early on and communicate it to AR or collections so that they can take the actions needed to resolve the issue.

Set the alert dollar limit to fit the size of your company. You don’t need to review every short payment, as that can be handled as a part of AR and Collections daily activities. You do want to review any material short payments though, as they are almost always a sign of a customer issue.

Successfully implementing a new process isn’t always easy. Consider the best practices below to streamline and control new process implementations.

When hiring new accountants be sure to include cash handling, transaction entry and the bank reconciliation process training as a part of their onboarding. Assign a temporary mentor from accounting to ensure that training happens.

System permissions and security functionality play a vital role in any ERP process. Using these “feature rich” ERP tools, allow the user to set up efficient and controlled processes.

A common cash transaction recording and reconciliation permissions example is displayed in the table below:

| Screen | View | New | Edit | Delete |

| Functionality | ||||

| Cash Accountant | ||||

| Cash and Bank transaction entry (No approval required up to defined limit) |

X | X | X | NA |

| Accounts Receivable cash application | X | X | X | NA |

| short pay processing (No approval required up to defined limit) |

X | X | X | NA |

| Bank Reconciliation Accountant | ||||

| Bank reconciliation functionality | X | X | X | NA |

| Bank reconciliation transactions (Import and manual entry) |

X | X | X | NA |

| GL journal entry (Cash and bank accounts) |

X | X | X | NA |

| Company Executives | ||||

| Cash and Bank transaction review (Above accountant approval limit) |

X | NA | NA | NA |

| Short pay approval (Above accountant approval limit) |

X | NA | NA | NA |

| Bank reconciliation review | X | NA | NA | NA |

| Measures and Alerts | ||||

| Cash Accountant | ||||

| None | ||||

| Bank Reconciliation Accountant | ||||

| JEs posted directly to cash GL accounts from outside the Cash sub-ledger. | X | NA | NA | NA |

| Company Executives | ||||

| Bank transactions more than “N” dollars. | X | NA | NA | NA |

| “Short pay” Accounts Receivable cash application transactions more than “N” dollars. | X | NA | NA | NA |

| System bank reconciliations not completed “N” days past period end. | X | NA | NA | NA |

Processing bank transactions in a timely manner is critical to supporting cash handling internal controls and cash planning activities. Transactions should be imported or entered daily. Remember, efficient processing not only supports transaction control and planning, but it can also be a factor in reducing cash loss.

Use the tools provided by the bank and your ERP. Use the capabilities to streamline cash transaction processing and increase transaction processing accuracy and control.

Talk to us about how Velosio can help you realize business value faster with end-to-end solutions and cloud services.

"*" indicates required fields